When you take out a home loan, it is possible to spend a predetermined matter per month (when you yourself have a predetermined rate financial: read on to find out more). It is a bit difficult to find out: our company is large fans of utilizing a mortgage calculator to make an guess. For individuals who simply want to ascertain your repayments, try this you to of the moneysavingexpert: we think it’s expert. If you want to understand how to determine mortgage repayments your self, continue reading!

Why is it therefore tricky?

It would be simple to find out a home loan fee if the newest number don’t change over date. Regrettably for us, they are doing-significantly. Financial institutions need to make currency off of the currency they lend, so that they charges interest toward that loan. Mortgage attention is actually the price the financial institution charge you to borrow cash.

There clearly was a vintage story one to Albert Einstein titled compound notice the most effective push in the market. If you’re we are not certain that it is value this much compliment, it is extremely effective. The phrase compound makes one thing more difficult for people. For those who obtain ?10,000 getting a decade during the dos% effortless desire, possible spend ?200 from inside the desire from year to year: that’s easy. not, for folks who borrow that have compound focus, we need to calculate the attention any time you build an effective https://cashadvanceamerica.net/payday-loans-nd/ commission.

- Your acquire ?10,000 in the 2% notice for five decades, having yearly money out-of ?2, (You are able to a beneficial calculator to test it. We have fun with Excel’s situated-for the PMT mode).

- The first season, you borrowed from the financial institution ?ten,000. It is possible to build a fees out-of ?dos,. You are spending dos% attract, very ?200 of the payment was attract, the other ?step 1, try dominant. (The primary is the count your debt to start with) The thing that makes the difference between interest and you may prominent essential? Focus happens to the lending company, you deduct the primary throughout the count you borrowed next year: ?ten,000-?step 1,=?8,.

- The next season, you owe the lending company faster (?8,). You can easily still make a payment off ?2,, but you’ll spend smaller notice this time. 2% out of ?8, is ?, and rest (?1,) goes to the primary. So now you owe the financial institution ?6,.

- Seasons around three, you create an identical fee away from ?2,. Now, you pay focus out-of dos% on ?6,: so it concerns ?. At this point you are obligated to pay ?4,

- 12 months five, repeat: 2% from ?4, was ?. So now you owe ?2,.

- 12 months four (in the long run!), you create the last percentage: ?2, along with dos% focus sums around a neat ?2,. Find exactly how here is the direct sized the commission-that’s what helps to make the algorithm useful.

Challenging, best? This will be along with the reasoning interest levels are incredibly crucial: should you have an excellent 5% interest from the more than example, might pay nearly ?step one,000 so much more during the desire. Envision what might happens whether it had been an effective ?eight hundred,000 home loan more than 25 years! (Hint: it is not very)

What about adjustable rates?

We’ve been talking about repaired pricing up until now, in which the interest rate does not change. For the a changeable rates home loan, your own rate of interest changes, will at impulse of the bank. Always, it adjustable speed is dependent upon the lending company out-of England’s bank price, and additionally 2 or three %. On the a fundamental varying rates, the lender have total control of the rate of interest.

For people who consider material focus is difficult, changeable prices was absolutely devilish. Very financial institutions simply quotation a prices having testing: this is exactly a knowledgeable assume regarding exacltly what the mediocre interest rate will be for individuals who remain on that mortgage. These types of educated presumptions go for about as effective as we can create: in the event you learn how to expect rates precisely, call us. (It’s very tough.)

This is very important since the majority mortgages keeps a fixed speed to possess a brief period: 2-5 years, normally. A single day their mortgage leaves that it introductory price, you’ll be using an adjustable speed, and your repayments can transform monthly!

With the maths-more likely among us, the borrowed funds payment algorithm isn’t that difficult. Keep in mind, this does not be the cause of variable rates, that alter.

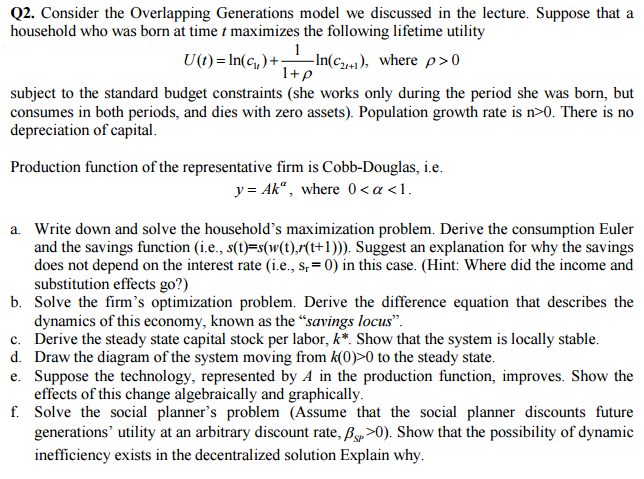

- r = Annual interest (APRC)/a dozen (months)

- P = Prominent (doing equilibrium) of your own mortgage

- n = Amount of payments as a whole: if you make you to mortgage repayment per month to own 25 years, that is twenty-five*12 = 3 hundred

If you fail to give in the products a lot more than, that is a ?350,000 financial on step three.3% APRC and you can a twenty-five-season term.

OnLadder try a friends entered within the England and you may Wales under registration amount 12677436. All of our entered office try 71-75 Shelton Street, London area, England, WC2H 9JQ.